Average retirement savings for U.S. households was $255,000 in 2019. This guideline provided by Fidelity include the savings you have in your retirement account such as 401k/403b, Roth IRA and your company matches or defined contributions. These savings milestones by age will help you stay on track for retirement.

Milestones

This guideline is based saving so that you can live on 80% your pre-retirement income. I don’t know if it’s a perfect solution but I do think it’s important to have milestones, just as there are milestones for our children. If you have kids, you know that if your kid is not walking by age 1, you need to pay attention. Savings milestones do just that. If you haven’t met it, you need to pay attention and see what you can do to correct the course.

Savings by Age

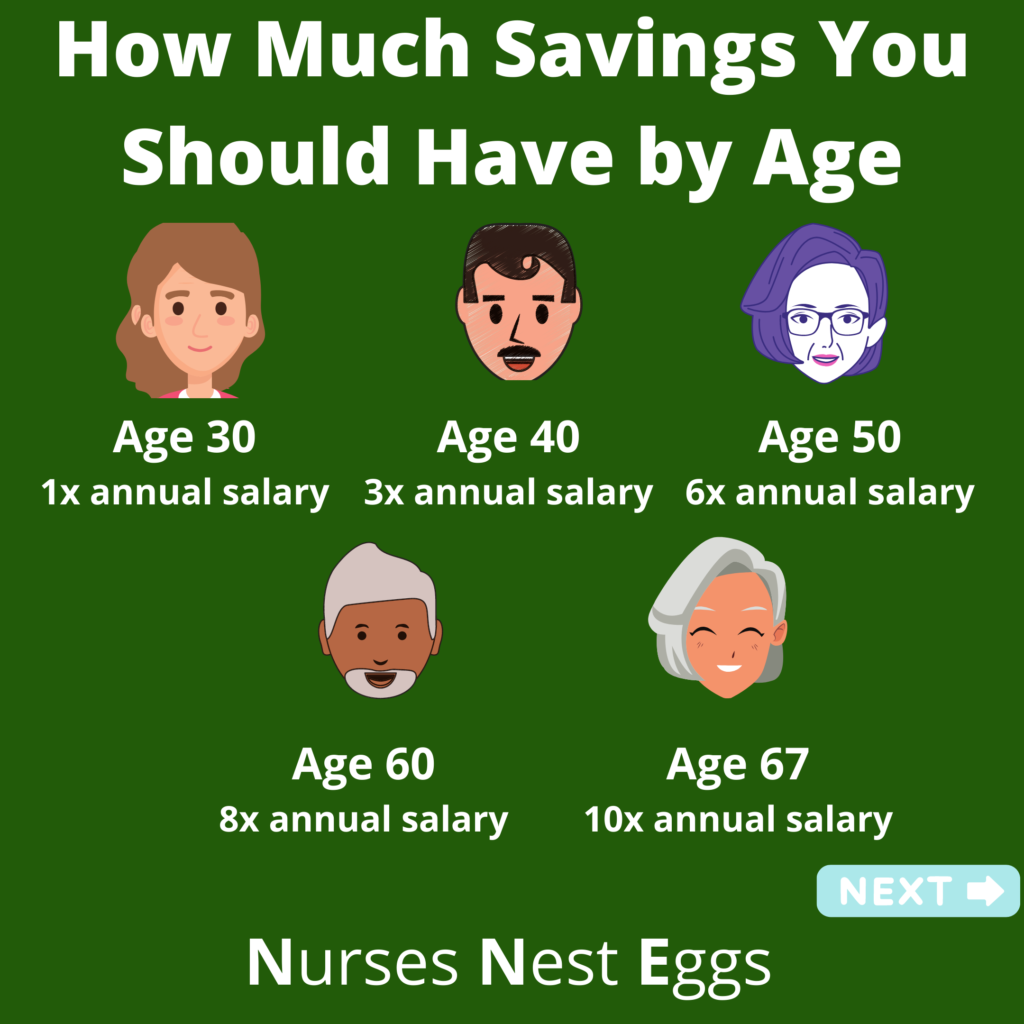

30: 1X your income

40: 3X your income

50: 6X your income

60: 8X your income

67 or retirement: 10X your income

Savings Milestone by Age 30

You should have 1x your annual salary by age 30. Maximize your income by working over time. Say “yes” as frequently as you can. Your goal should be to make as much money as possible while you can. If you’re the best nurse on your unit, you will be promoted. This is the mostimportant part of your journey to financial freedom because you can cultivate savings habits early on.

Habits

What you do in your early years will determine whether you will have enough money to retire early. First, you will be nurturing the habits of not spending your money frivolously, saving, and managing your personal finance. Second, the earlier you start saving, the more time you have for your money to work for you.

Compound Interest

Imagine you are 60 years old. If you have $100,000 and your annual return is 10%. You’ll have $110,000 by the end of the year. You would have gained $10,000 in one year. Imagine if you have $1 million, you’ll have $1.1 million by the end of the year. You would have made $100,000 in a year, which is twice the income of an average American. You will not get to a $1million, unless you start when you are in your 20’s-30’s.

I know it’s hard for young adults to imagine having $1million but it is definitely possible and doable.

“Compound interest is the 8th wonder of the world.” -Albert Einstein

Lessons for 30's

Make more than you spend

Cultivate savings habit

Invest aggressively

Take risks

Savings Milestone by Age 40

This may be the most difficult decade to save due to the fact that you may be sending your kids to college. Your wallet is always open since we cannot say “no” to people we love. If you haven’t saved enough, consider having your kids pay a portion of their tuition. Be patient during this decade.

If you weren’t able to reach your milestone of saving 1x your annual salary in your 30’s, you still have time to catch up. You should have three times your income in your 40’s.

Optimize Your Earning Potential

Due to factors mentioned above, this is the decade to optimize your earning potential. You have experience and wisdom on your side. Reach high for the promotion that you deserve. Not only will it increase your income, you will not regret the lessons you learn as a leader.

Side hustles during this decade can also help you earn more money to pay a portion of tuition, save money for an emergency fund or contribute to your retirement fund.

Lessons for 40's

Be patient during this decade

Optimize your earning potential by promotion

Start a side hustle

Savings Milestone by Age 50

By age 50, you should have six times your annual salary in savings. This is the decade when your kids would graduate from high school or college. If you spent extra money on your kid’s tuition, you should be able to now put that money towards your savings. Once my daughter finished college, I was able to contribute the maximize into my savings. Saving aggressively allowed me to invest in two more rental properties.

Retirement Plan

Make a detailed plan on how to fund your retirement if you haven’t already. Late 40’s or early 50’s are when people start to think seriously about retirement. You don’t want to start planning late to find out that you don’t have enough money saved to retire.

Downsizing Your House

After your kids leave the nest, you may also be able to downsize your home. In my 50’s, I downsized my house and paid off all the debt. In addition, I was able to stash some cash for emergency savings account. With the proceeds from selling my big house, I purchased two more houses. Being at the height of my career with experience and a little more wisdom on my side helped me earn more income.

Lessons for 50's

This is the decade when you can save the most

Invest aggressively

Make a plan for retirement if you haven’t already

Savings Milestone by Age 60

This is the decade when you have to get ready for retirement. I haven’t hit 60 yet but I’m close. The year 2020 has taught me that you have no idea what God and nature have ensured for us. The stock market is over valued and the prediction from the smartest people is that it will crash hard. If you have contributed to your retirement fund like I did, there is no way to escape from the stock market.

Managing Retirement Fund

With the low interest, bonds are not able to provide adequate return for the retirees. Therefore, I sought out dividend paying stocks. If you pick the right stocks or ETFs, they can deliver adequate returns. For example, if your stock pays 3% in dividends, you would make 3% even if the price of the stock doesn’t go up. Anticipate and invest accordingly. This is the decade in which you really have to learn to invest to make your hard earned money work for you.

Real Estate Assets

If you own your home and are close to paying it off, you will be in good shape. Investing in real estate early on and paying it off by the time you retire should give you added income and security.

Lessons for 60's

Make more than you spend

Invest in dividend paying stocks

Put your retirement plan in motion

Savings Milestone by Age 67

This is the age most of us will reach the full retirement age. You should have 10x your annual salary saved by this age. Let’s say your income was $80,000 by the time you retire, which is $800,000. You can withdraw 4%, which is $2,666 per month. Adding Social Security income should give you the monthly income you need. Talk to a financial advisor or an account to make sure you get the maximum amount of Social Security income. Paying off your house or having a rental property, can also add to your overall retirement income.

Invest for 20 Plus Years

Over 40% retirees said their greatest fear was running out of money. A lot of financial advisors overemphasize bonds. Yet, the current bond yield will almost guarantee you’ll run out of your savings. Chunk up your money into thirds. Invest one third conservatively, which you will use in the first 10 years of retirement. Allocate the second third into moderate and the last third into aggressive investments.

Lessons for Age 67's

Keep investing

Bear in mind that your retirement fund has to last 20-30 more years